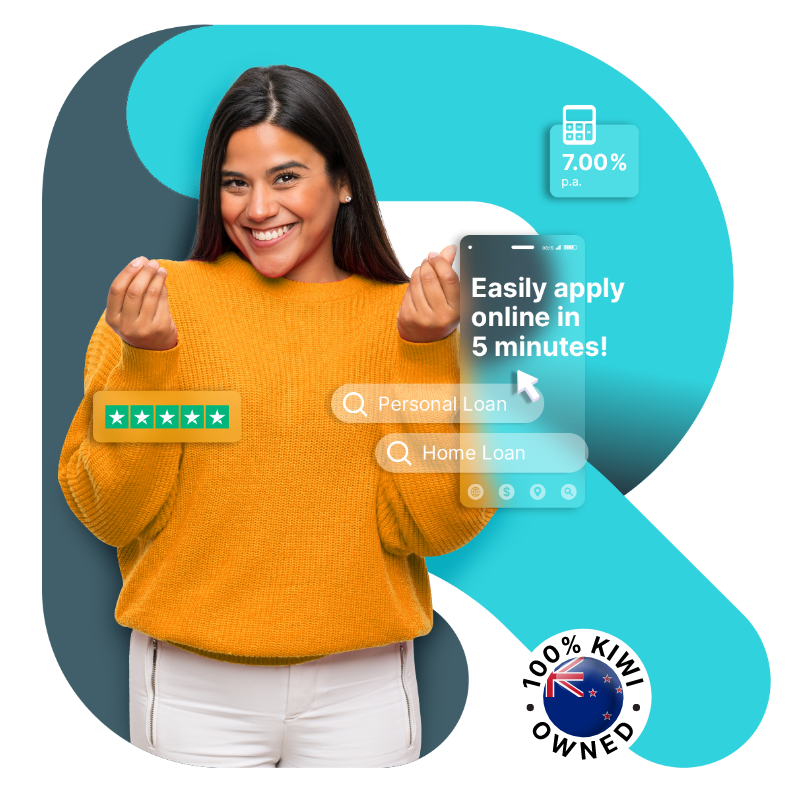

RATES

from 7%

NZ OWNED

and operated

RANGE OF LOANS

to fit your needs

Personal Loans

We will create a personalised loan for you from 9.95% p.a. for those unexpected life events.

Debt Consolidation

Tired of juggling debt?

We help you take control of your finances with one easy repayment.

Vehicle Loans

We make applying for vehicle finance simple so you can buy that car, motorbike, boat, jetski or motorhome.

Unsecured Loans

Unsecured loans from $1,000 to $50,000. We make applying for unsecured loans simple. Apply for an online loan today.

Home Loans

Buying a home is exciting! Whether you are buying your first home, an investment property or simply refinancing, apply online today

Business Loans

Personalised lending solutions for your business. If you are looking to buy Plant and Equipment or just require working capital, let’s chat!

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua.